AI · SEO

The 2026 SEO Visibility Map for Australian Aged Care

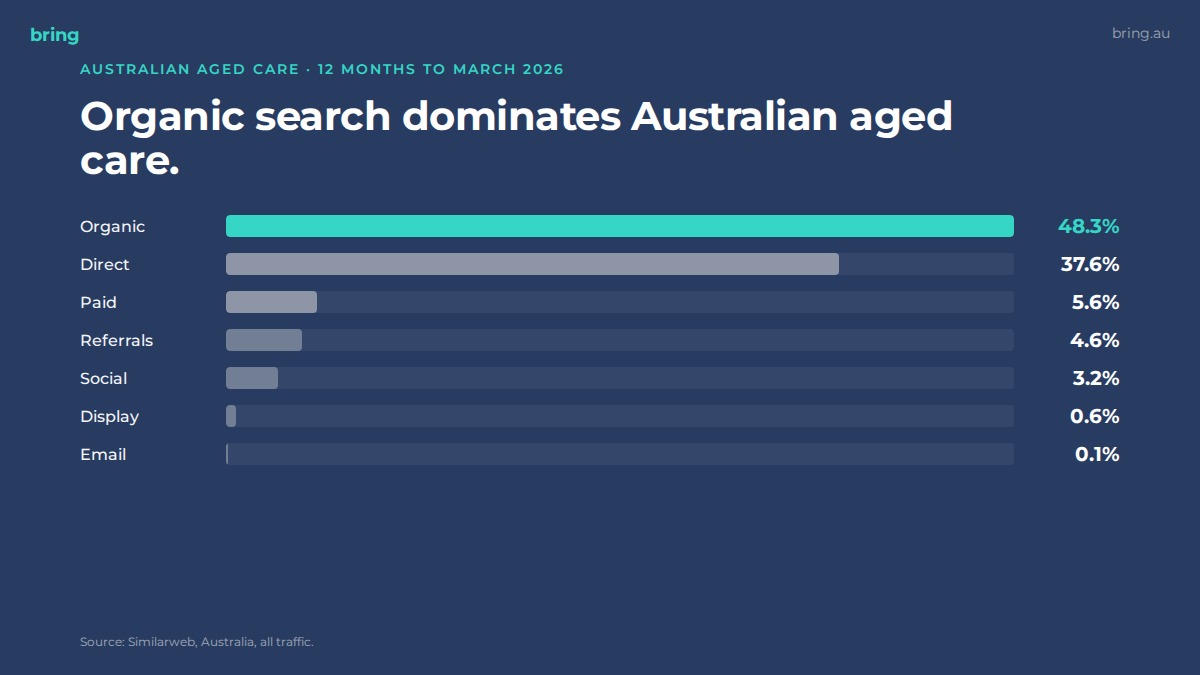

48% organic, 5.6% paid. The 12-month aged care SEO data, the providers gaining share, and the ten opportunities most providers are missing.

Organic search dominates Australian aged care. 48.29% organic, 5.6% paid.

The structural mix favours providers who invest in authority over spend.

Most providers have not noticed.

We’ve pulled 12 months of Similarweb data, the keyword landscape, AI search positioning, and the conversion patterns of every top-30 provider into a single view. The picture is clearer than the category usually allows. Some providers are gaining share rapidly. Others are losing it just as fast. The gap is widening every quarter, and the 2026 reform calendar is about to widen it further.

This article covers the headline shifts and the ten opportunities most providers are missing. The full 18-page report sits at the end if you want the named providers, the keyword data, and the conversion architecture analysis.

Aged care digital marketing in 2026, by the numbers

Australian aged care websites pulled 28.55 million visits in the 12 months to March 2026, down 3.79% on the prior 12 months. That headline figure looks soft. The deeper numbers say something else.

Unique visitors grew 14.05% year on year, to 740,955 in March 2026. Pages per visit grew 29.06%. Visit duration grew 16.04%. Buyers are entering the category later, doing more research per session, and converging on fewer trusted sources. They are not searching less. They are searching more deliberately.

Australian Institute of Health and Welfare reporting confirms the underlying demand. Government investment hit $39.2 billion in FY25, up 9.6%. KPMG’s 2026 Aged Care Market Analysis forecasts continued growth and continued consolidation, with the top 25 residential providers now controlling 44.7% of operational places. The aged care market is forecast to grow from US$34.4 billion in 2025 to US$61.3 billion by 2034, a compound annual growth rate of 6.43%. The demand is structural and growing. The question is which providers capture it.

Why aged care SEO matters more here than anywhere else

Channel mix in any category tells you what the buyer journey looks like. In aged care, organic dominates: 48.29% of traffic, against 37.56% direct, 5.6% paid, 4.63% referrals, 3.21% social, and 0.07% email.

That ratio is unusual. Most service categories sit in the 25 to 35% organic range, with paid contributing 15 to 30% of traffic. Aged care is structurally different. Buyers in this category cannot be acquired with a clever ad. They are researching what care is, who their parent qualifies for, what the assessment process involves, and what trust signals to look for. They are doing this work over weeks and months, not minutes.

That makes aged care a content category. The providers who win are the ones who answer the questions buyers are actually searching for, on pages that work for both Google and the AI systems that increasingly handle the first-stop discovery layer. The providers who lose are the ones treating their website as a brochure and their paid budget as a substitute for content. We made a similar argument in our prior aged care landscape analysis, and 12 months later the data has only sharpened the case.

61.54% of traffic in the category is mobile, against 38.46% desktop. Any aged care SEO or digital marketing strategy that does not centre mobile-first conversion architecture is structurally disadvantaged.

The growth-decline split

The most informative data point in the category is the 12-month change in visits across the top 30 sites. The gap between gainers and decliners is large and growing.

Among gainers: Arcare grew 157%, Feros Care 113%, Bethanie 72%, Amana Living 67%, Opal HealthCare 44%, Bupa Aged Care 35%. These providers vary in size, ownership structure, and geography. They share three things.

First, strong location-page coverage. Each of the gainers has restructured their residence or service-area pages with full local schema, local context, and bookable tours. Arcare’s residence pages are particularly strong, with weekend tours surfaced as a deliberate conversion mechanic.

Second, educational content for high-intent process queries. Bethanie’s “How to Choose the Right Aged Care Provider for Your Needs” article, published in March 2026, ranks in AI search results across multiple major LLMs for the equivalent query. Feros Care’s Support at Home content cluster covers the eight new funding classifications, the transition from Home Care Packages, and the practical implications for buyers. Both are taking ground that the government domains have historically owned.

Third, relationship-first conversion language. Arcare uses “Care Community” rather than “facility”. Bethanie leads with empathetic, journey-oriented framing. Feros Care leads with values and pricing transparency. Each respects the emotional weight of the decision rather than treating aged care as a logistical purchase.

Among decliners: Benetas lost 71%, Regis lost 47%, Brightwater lost 35%, Aveo lost 27%, AgedCareOnline lost 22%. The pattern across these brands is the inverse. Corporate scale language, generic CTAs, location pages without distinctive content, weak engagement with the Support at Home transition. Regis still uses “Find a location” and “Book a tour” without specificity. The data suggests this is not enough in 2026.

The Support at Home content gap

The Support at Home program took effect on 1 November 2025. It replaced Home Care Packages and the Short-Term Restorative Care Programme. It introduced eight new funding classifications, replacing the four HCP levels. It is the most consequential policy shift in Australian aged care in a decade. The Department of Health, Disability and Ageing’s Support at Home overview remains the authoritative source on the program structure.

Search behaviour has followed. Combined annual traffic for “support at home” and “support at home program” sits above 3,700 monthly visits. Volume is growing month on month as buyers entering the system after November 2025 search for the new program rather than the legacy HCP terminology.

87% to 90% of that traffic goes to government domains. health.gov.au and myagedcare.gov.au absorb almost all of it. Among the top 30 private providers, only Feros Care has built ranking content that captures meaningful share of Support at Home queries. Every other provider is largely absent from this surface despite their commercial dependence on the program.

This is the largest content vacuum in the Australian aged care category. The window to claim authority is open, and it will not stay open. From 1 July 2026, government-set price caps apply, and the May 2026 Budget allocated $3 billion in additional aged care investment, including $1 billion to make personal care services free of charge under Support at Home from October 2026. Each of these reforms will trigger another wave of search behaviour. Providers who own the Support at Home content layer now will compound their authority across each subsequent reform cycle.

The aged care AI search window is open

ChatGPT, Gemini, and Perplexity now answer “best aged care provider” queries, “how to choose aged care”, and “aged care home Sydney” queries for an increasing share of buyers. The brands they surface are not the same as the brands ranking on Google.

Government domains dominate AI surfaces in this category. myagedcare.gov.au, agedcarequality.gov.au, health.gov.au, and aihw.gov.au are cited consistently across all three major LLMs for category-trend, process, and comparison queries. Private provider brands surface inconsistently. Some providers (Bethanie on the “how to choose” prompt, BlueCare and TriCare on the “how do I get my parent into aged care” prompt) are starting to appear, suggesting that targeted educational content can earn AI authority.

Most providers are not yet structuring content for AI discovery. The work to do is specific. Schema markup applied consistently across pages. Author bios with E-E-A-T signals. FAQ formatting for conversational query handling. Cross-domain entity consistency, so the provider’s name, locations, services, and accreditations form a coherent entity graph. None of this is exotic. All of it is overdue. We covered the underlying behaviour shift in changing search behaviours for aged care and retirement living.

The compounding effect is real. AI surfaces reward early entrants. The brands surfaced today shape the brands surfaced in 12 months. Providers who claim AI authority now will hold disproportionate share when AI-driven discovery becomes the dominant first-stop search behaviour, projected to be by 2027.

Ten opportunities most aged care providers are missing

The full report covers ten ranked opportunities by commercial leverage. The first five summarised:

- Support at Home content authority. Build a content cluster covering the program at category, service-tier, and transition levels. 87% to 90% of category traffic for these queries is currently captured by government sites.

- ACAT and assessment educational content. ACAT-related queries pull over 10,700 annual visits. The assessment is the gateway moment for every aged care purchase decision.

- Local SEO and “near me” capture. Restructure each residence page as a local landing page with full LocalBusiness schema, GBP integration, and individual residence-level content.

- Star Ratings as a content asset. Surface Star Ratings as a primary trust signal on every residence page. From April 2026, ratings affect a portion of provider funding.

- AI search positioning. Restructure content for entity recognition and LLM citation. Schema, author bios, FAQ formats, and cross-domain entity consistency.

The remaining five cover dementia and specialist care content, fee transparency, carer and family support content, provider comparison content, and lead capture flow optimisation. Each is detailed in the full report with the gap, the angle, and the commercial outcome.

What this means for aged care providers in 2026

Aged care is moving on three fronts at once. Reform is rewriting the language buyers use. AI search is rewriting where buyers look first. Conversion architecture is rewriting which providers convert that attention into enquiries.

The brands gaining share in 2026 are responding to all three. The brands losing share are responding to none. The category is bifurcating, and the position you hold by January 2027 will be largely set by what you do in the next two quarters.

The full Aged Care Intelligence Report 2026 covers the visibility data, the keyword landscape, the AI search test results, the conversion pattern analysis, and the ten ranked opportunities in detail. 18 pages. Free to download.

Download the full report

The 2026 Visibility Map for Australian Aged Care. 18 pages of data, named providers, and the ten opportunities most providers are missing.

Get the report